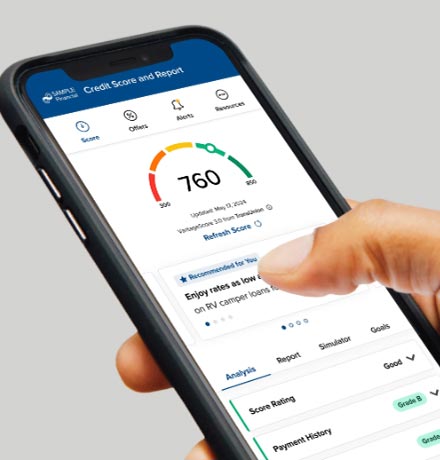

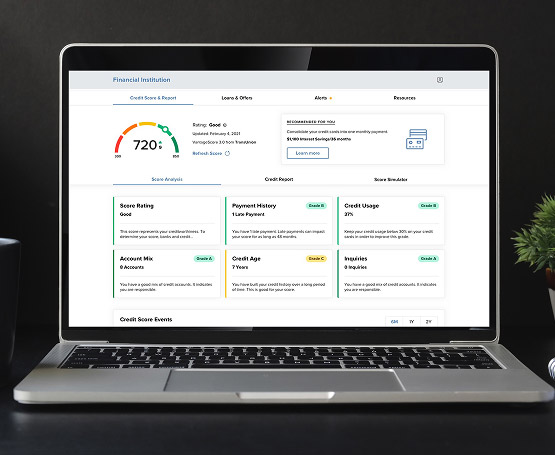

SavvyMoney empowers you with the tools to understand your finances and set financial goals!

SavvyMoney allows you to:

- See a summary of your credit report without a hard pull

- Use the Score Simulator to estimate how certain actions will affect your credit score

- Take a financial assessment to gauge your current financial habits

- Set a credit goal and track your progress

- Receive recommendations from SavvyMoney to meet your goals

How to Enroll:

- Login to your Digital Banking account.

- Click the SavvyMoney widget on the right side (desktop) or underneath your accounts on your dashboard in the mobile app.

- Allow SavvyMoney access to your credit score and start receiving real-time credit score updates and alerts!

Don't have Digital Banking? Register Now!

FAQs

What is a credit score?

A credit score is a three-digit number calculated to indicate your creditworthiness. The higher the score, the more creditworthy you are to a lender. A credit score is calculated from the information in your credit report and takes into account whether you have been making on-time payments, your revolving debt use, the length of your payment history, and other such factors. It is important to note that your score does not take your age, income, employment, marital status, or bank account balances into account.

What is a credit report?

Credit reports, also known as credit files, are composed of the credit-related data a credit reporting company has gathered about consumers from different sources. Credit reports include records of mortgage payments, credit card balances, credit card payments, auto loan payments, and credit inquiries. It may also include accounts that have gone into collections, public records, and other information from government sources.

What does a good credit score mean to me?

A good score may mean you have easier access to more credit and lower interest rates. The consumer benefits of a good credit score go beyond the obvious. For example, underwriting processes that use credit scores allow consumers to obtain credit much more quickly than in the past.

How do I improve my credit score?

There are several ways to improve your credit score. But it’s much more important to focus on improving what’s in your credit report rather than obsessing over your credit score. Here is some general advice:

- Pay your bills on time. How promptly you pay your bills has the strongest influence on your credit score.

- Apply for credit only when you need it. Do not open too many accounts too frequently. And avoid opening multiple accounts within a short time span.

- Keep your outstanding balances low. A good rule of thumb? Keep balances below 30 percent of the credit limit on each of your revolving accounts.

- Reduce your total debt. It is not necessarily bad to owe some money. But it is not good to owe too much money. Consider paying down some of your outstanding loans.

- Build up a credit history. Maintaining a timely payment history for a mix of accounts (e.g. credit cards, auto, mortgage) over a longer period can improve your score.

What is a Debt-to-Income Ratio (DTI)?

Your DTI is a simple number that shows how much of your monthly income goes toward paying off debts. It helps you understand if you’re taking on more than you can afford.

Why does my DTI matter?

Your debt-to-income ratio is a snapshot of how well you’re balancing your debt and income. A high DTI can make it harder to get approved for things like loans or credit cards, while a low DTI usually means you're in a stronger financial position.

What counts as "debt" in DTI?

Anything you’re required to pay each month—credit card minimums, student loans, auto loans, mortgage or rent, and even personal loans. It doesn’t include things like groceries, utilities, or subscriptions.